Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Retire successfully with Informed Decisions.

20th February 2023

Choosing a Financial Advisor in Ireland is not an easy task! There are many different types of advisors, operating in different ways, being remunerated differently, and all delivering different services.

And to be clear; I am a firm believer in good financial advice. I believe it is worth so much more than it costs, when done well. I am an ardent advocate for Financial advice in Ireland, and my efforts are made in order to try to improve how it is done so as to benefit us all.

So, in this piece, I will share with you;

If you prefer bullet points, feel free to skip to the summary at the end of the piece!

This piece was triggered thanks to a question from a friend about a recent article I posted on LinkedIn, relating to Blog193, Can you trust your accountant? In that piece, I questioned the validity of ‘Investment Advice’ that many people get from their accountants and other sources in Ireland.

While a tiny bit risque and tongue-in-cheek, I do hope this is an interesting and informative piece.

In Blog96 here (4 years ago now!) I detailed how to get Independent Financial Advice in Ireland, and an overview of the different types of financial advisors in Ireland at the time.

Not a lot has changed to be fair, though some aspects of service from each have shifted over the 4 years. In no particular order, here are the main types of Financial Advisor in Ireland, how to spot them, and how they are paid!

Social Media Individuals: There is a growing cohort of unregulated financial ‘advisors’ on TikTok, Instagram, YouTube, Facebook etc. For a long time, I thought this was a ‘USA-thing’ only, but there are Irish versions popping up all the time! Most of these are unregulated, have minimal qualifications or experience actually giving advice or knowing the broader context of what they speak about.

Their primary objective is usually to get as many ‘views’ as possible. As a result, they often talk about whatever is fashionable this week, crypto etc. etc.!

They usually don’t actually offer a personal advice service. Instead, they generate income from links that you click or anything you buy as a result of clicking affiliate links on their pages. While there are some exceptions, such as Fritz Gilbert’s excellent Retirement Manifesto Blog, I tend to suggest steering clear of most ‘influencers’!

Bank Advisors: Easy to spot because they will be sitting in an office in your local bank branch! Bank advisors are paid a (usually decent) basic salary to talk to bank customers about their financial needs. They have well-drilled and prudent sales processes that they (should) bring customers through, to determine if there is a real need for a financial product (pension, investment, protection) or not.

Bank branch staff are encouraged to send you into these advisors when they sense an opportunity, such as when you lodge or withdraw a large sum into your accounts, or have large balance on your business account.

Like anyone, these advisors are under certain expectations from above to deliver sales of the products they offer. They don’t generate anything, and won’t be deemed successful unless you buy something from them.

Most of them also stand to make bonuses if they hit certain sales targets. In my experience, though, the majority of them tend to be relatively new to the profession, haven’t been corrupted by greed, and have the interests of the customer at heart.

Insurance Brokers: This one needs some context! Prior to April 2020, any advisor in Ireland with agencies to sell insurance products from a multiple of the main insurance companies could call themselves ‘Independent’.

For example, if a broker sold pensions/protection/investment products on behalf of say 5 different insurance companies, and received various commissions from each of these companies, up to April 2020, they called themselves an Independent Financial Advisor.

As of 1st April 2020, under Central Bank of Ireland rules, for an advisor to be allowed to refer to themselves as providing ‘Independent Financial Advice’ in Ireland, they must not receive any form of commission from any provider. As a result, most insurance brokers, who used to call themselves ‘Independent Financial Advisors’, are now using the title ‘Financial Planner’, which confuses things!

The reality is that the vast majority of non-bank financial advisors and advice firms in Ireland are insurance brokers, in the eyes of Central Bank of Ireland. It’s neither a positive or a negative; it’s a fact.

They sell insurance company pensions, investments and protection policies to people who seek their help in sourcing such things.

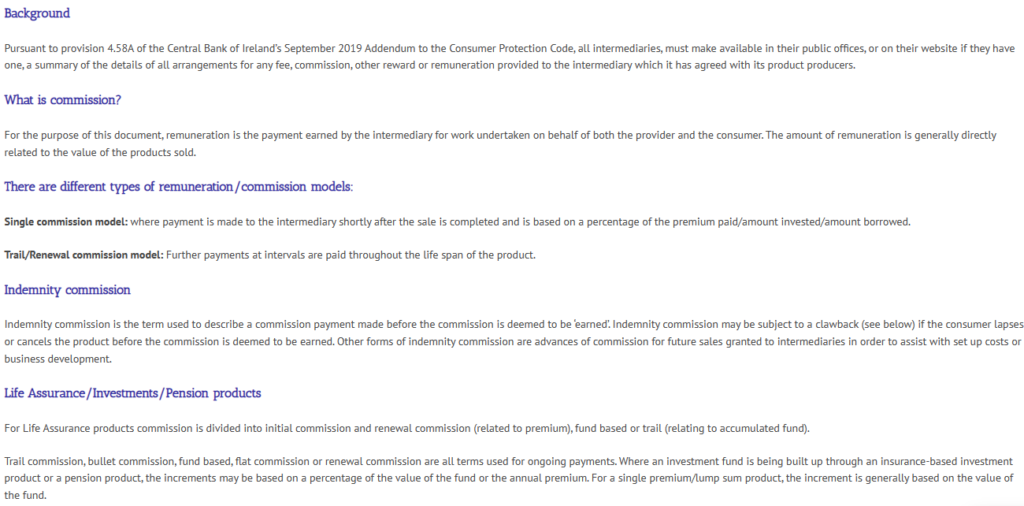

In 2019 an addition to the Consumer Protection Code (the Code which all regulated firms must adhere to) obligated any financial advisor firm in Ireland to declare commission incomes they could potentially receive from insurance companies, for the sale of products. They are obliged now to put this on their website.

You can tell if a firm sells such products in return for commission from an insurance company(ies) by looking at their website.

Any firm that receives commission is obliged under Central Bank of Ireland rules to put a ‘Remuneration’ page on their website, to show the rates of commissions they can get for the sale of insurance products. If you look at the website of every Financial Planning firm or Financial Advisor in Ireland, you will see a section or tab, usually tucked away in the bottom, titled ‘Our Remuneration’ or ‘Charges’.

If you want to know if a firm you are evaluating receives commissions, click that link, and if you see the following generic wording, you have your answer. They are obliged to put this generic wording on their website if they receive commissions:

Very simple way of knowing whether they are truly fee-only or not.

So, if a financial advisor in Ireland sells insurance products in return for commissions, does that make them bad advisors? I don’t believe it does.

Just as a doctor will prescribe medications, a financial advisor should only suggest certain products to you if they believe/know that they will help you execute a plan, to achieve a goal, or to avoid a financial loss.

Anyone who has watched the incredible OxyContin Docuseries Dopesick, or who knows the influence that doctors can be under from pharmaceutical companies, will acknowledge that very few professions are free from conflict.

And this is where it gets tricky in choosing a financial advisor in Ireland too!

If we work on the accurate basis that the vast majority of regulated Financial Advisors in Ireland, and firms, are ultimately Insurance Brokers selling insurance products in return for commission, how can you determine who will, or can, deliver a certain service to you!?

If we take a fictional sample of 100 financial advisors in Ireland, I’ll guess that about 50 of them clearly refer to themselves as ‘Insurance Brokers’ – they are open about focusing on selling insurance products to you, and deliver the products that you need, hopefully at a fair price and in a speedy fashion. They don’t promise anything else.

Customers will usually recognise that the broker is getting paid a commission from the insurance company whose product you end up buying. Much like a brothel, the service tends to be quite transactional, and everyone knows what everyone else is in it for!

If you need a pension, they’ll give it to you. If you think you need Life Cover to protect your loved ones, they’ll help you get that in place too. And off out the door you go!

Of the remaining 50, there are approx. 30 who refer to themselves as ‘Financial Advisors‘. They might offer to do a little bit more investigation, discussion and planning with you, before going to the product sale. They might try and open the conversation, to see if there are other areas of your financial life, and, therefore, products you might need.

If we were to compare it, it might be similar to a male or female Escort; they’ll sit with you and chat through dinner, but really they’re just there to get the job done and get the money!

The poor customers in this scenario may or may not realise that their advisor is getting commissions from the insurance company when they buy a product or change their schemes with the advisor. They may think that they are paid by magic, or by some sort of other arrangement.

I repeatedly hear directly from people who, when they ask the ‘how are you paid’ question, are told that the insurance company pays for the advice, and that they don’t need to worry their ‘little heads’ about it.

Massively misleading and dismissive, as the client buying the product will ultimately pay the commission that the insurance gives to the financial advisor, through often-hidden fees and costs of the product. This is where the wolf in sheep clothing most often lurks! (See Blog 95 for more on this)

That leaves the final 20 advisors from our 100 sample.

Again, rough guesstimate here, based not on any hard data!

These 20 will call themselves ‘Financial Planners’, where their website will talk about ‘You’ and ‘Your Goals’ and your ‘Best Life’, as opposed to your money! Many of these may have called themselves Independent Financial Advisors, until Central Bank of Ireland prohibited any firm receiving commissions from using the term Independent.

The harsh reality here is that of the 20 that talk about ‘real financial planning’, I guesstimate that 15 of them are really only stringing you along!

They’ll go on a few dates with you, might even buy the drinks, but they are just after one thing, and one thing only! And once they get it, you’ll not hear from them again for a couple of years, until they get the urge to take you for another spin!

That leaves 5 of the original 100! Yes 5.

Though it is thankfully rising every year, slowly, I estimate that currently only about 5 of the sample of 100 financial advisors in Ireland actually do ‘real financial planning’. My definition being, where their initial sole focus is on developing a thorough financial plan for the client.

It is not about focusing on the sale of a product. It is about prioritising the clients needs before the advisor needs. It is about being selfless and not trying to shoe-horn solutions where there are better alternatives that you don’t or can’t provide.

It is a patient and caring focus on the person, helping to figure out how to optimise their incomes, expenses, taxes, financial wishes, lifestyle preferences and emotions. That’s the first important role of a ‘real’ financial advisor in Ireland.

You don’t develop a financial plan in a 20-minute chat! It takes a lot of time, conversation and tweaking to develop a detailed financial plan that makes sense and that people buy-into. Only then, if a product or alteration is needed, should that be explored, discussed and analysed.

That, to me, is real financial planning in Ireland today. It is comparable to your chosen companion in life – they had to pass the test, they had to be with you in good times and bad, and only then did you know that they were the right one for you!

Before we get on any high horse, let’s acknowledge that financial advisors, like the oldest of professions, are in business! Financial advisors in Ireland have to generate income. And that’s part of the challenge within the current reality of the providers, advisors and interests at play in Ireland.

The vast vast majority, I estimate 99%, of financial advice firms in Ireland don’t generate any revenue from chatting with you or telling you what you should do, unless they sell you a product.

Until that changes, I don’t see how the service/motive/reality can or will change.

Commission-based advisors tend to (but not always) belong in 1 of 2 camps; up-front merchants and trail-builders.

‘Up-front merchant’ refers to advisors that take the very maximum up-front commission on offer from an insurance company. If that was say 5% on a lump-sum product, they might look to get €5,000 for selling you a €100k investment product, or €50,000 from a €1m product!

Once you buy the product, they get paid the commission, and unless you buy something again from them, you are not value to them. They don’t get paid anything else after year 1, unless you buy more. You can see why service might drop off the cliff after you have bought the thing you bought if your advisor pursues this model!

Traditionally, some of these advisors were known for ‘churning’ their clients. That is the act of maxing the initial commission, and then a few years later, when there were no commission claw-backs, tell the customer that they actually now have a better investment product available and that they should switch into this new one.

And yes, the advisor in question would look to get another 5% commission from the switch that they instigated. It’s funny but really not funny also. Clients end up paying these commissions through product fees, and all advisors get a terrible name.

This stuff still happens, and some of the most high-profile firms are actively doing it to drive up business value, drive crazy revenues and it’s the client and profession that loses out.

Trail-Builders are insurance brokers/advisors/planners that deliberately reject the large up-front commission, and instead opt for the insurance company to pay them a smaller amount each year over the future of the product, whether that is expected to be 5 or 50 years.

It usually doesn’t end up being any cheaper for the customer, but it does typically point to an advisor that is not going to simply treat you like an animal, milking you for all they can and cast you to the side. They, too are building a business of course and one with a solid going concern, but they tend (not always!) to be more customer-focused and offering real support to clients on an ongoing basis.

There are a slowly-growing number of firms who are regulated insurance brokers receiving commissions but are now also charging stand-alone fees for helping clients to formulate a plan or analyse their situation.

This is wonderful to see. Indeed, at Informed Decisions, quite often someone will seek our help but it becomes clear our service is overkill for their situation. We can and do direct them to some of these firms that provide this service. Nothing in it for us, but we’re delighted to help people who sought our guidance, and to help them avoid some of the less scrupulous advisors out there.

Only once they have worked on developing a proper plan, should there be a conversation about implementing any changes or buying any products. For a lot of people, I believe they really shouldn’t buy a product or implement any changes, until they have at least some form of clear and actionable plan that warrants that financial tool to implement it. That, I believe, is a key action required of a financial advisor in Ireland, no matter what form they take.

At Informed Decisions we only support clients on an ongoing (fee-only) basis after they have engaged us to complete a paid MasterPlan. This is a fairly engaged and deep process, to help chart a course for a client’s financial decisions and future. The reality is that not everyone wants to engage in that, or pay the fee!

We have in the past, and will in the future lose potential clients that don’t want to work with us in developing that initial plan. And that is OK by me, as we are committed to ‘No Plan, No Portfolio’ for every client. Sticking to that results in more clarity, more peace-of-mind and better results over the long term for clients.

In addition, being independent we don’t sell any insurance products. It doesn’t happen very often but if a client does need protection policies, for example, in order to complete their plan, we can direct them to a separate vetted expert in that field to get x, y or z sorted.

They complete that transaction separately with that insurance broker quickly and cost effectively. We deliberately don’t receive any kick-back on commissions, and the client has what they need. That’s a positive from an Independence perspective, but I also acknowledge it is less seamless for the client than it would otherwise be if we were not independent!

It’s easy for me to say all this of course. I was fortunate to be able to deliberately build a business to operate independently of any product, from Day 1.

And I know that if Informed Decisions was currently an insurance broker business where our revenue stemmed from commissions for selling insurance products, it would be very difficult to say goodbye to that income! I empathise with any firm now wishing to fully convert from a commission model to an independent fee-only model.

And it’s funny, if you google ‘Independent Financial Advice’ in Ireland, you’ll get hundreds of results, yet only 1 of them in actually independent as of today – just shows we can’t rely too much on what google results spit out, no matter the topic!

There are a few key nuggets I would love to make very clear here, in the hope it helps you:

I do hope this (cheeky, but fact-based) piece helps you, and ultimately the progression of financial advice in Ireland.

Paddy

Informed Decisions are one of Ireland’s only remaining independent financial advice firms. We specialise in retirement & investment planning for successful individuals, so that our clients only have to retire once.

Privacy Policy | Cookies | Disclaimer

Receive informed financial advice straight to your inbox every week with my newsletter.